Accelerated Death Benefits (ADB): Accelerated Death Benefits are an optional rider or provision added to a life insurance policy that allows the policyholder to utilize part or all of the death benefit while they’re alive.

Accrued Interest: Interest that has accumulated on a policy’s cash value, but has not been paid out. Alternatively, this can also apply to debt if a policyholder takes a loan on their policy.

Agent: A representative from an insurance company who evaluates your circumstances to help you choose a policy and negotiate the details of your contract.

Annuity: A life insurance payout option that provides money at a fixed amount on regular intervals, usually for the remainder of the policyholder’s life. The policyholder may pay premiums or a lump sum to the insurance carrier, which invests the money and provides tax deferred payouts on regular intervals.

Application: A form filled out by an individual when seeking life insurance coverage. The form serves as a statement of information about the policyholder to gauge health status and risk, which is used to determine eligibility and premiums

Assignment: The transfer of rights for an insurance policy from one individual or institution to another.

Beneficiary: An individual or group of people designated by a life insurance policyholder who will receive death benefit proceeds following the policyholder’s death.

Carrier: The company who issues a life insurance policy and provides coverage.

Cash Value: The investment component of an insurance policy, in which money accumulates over time and gains interest with the intention of being used later in life.

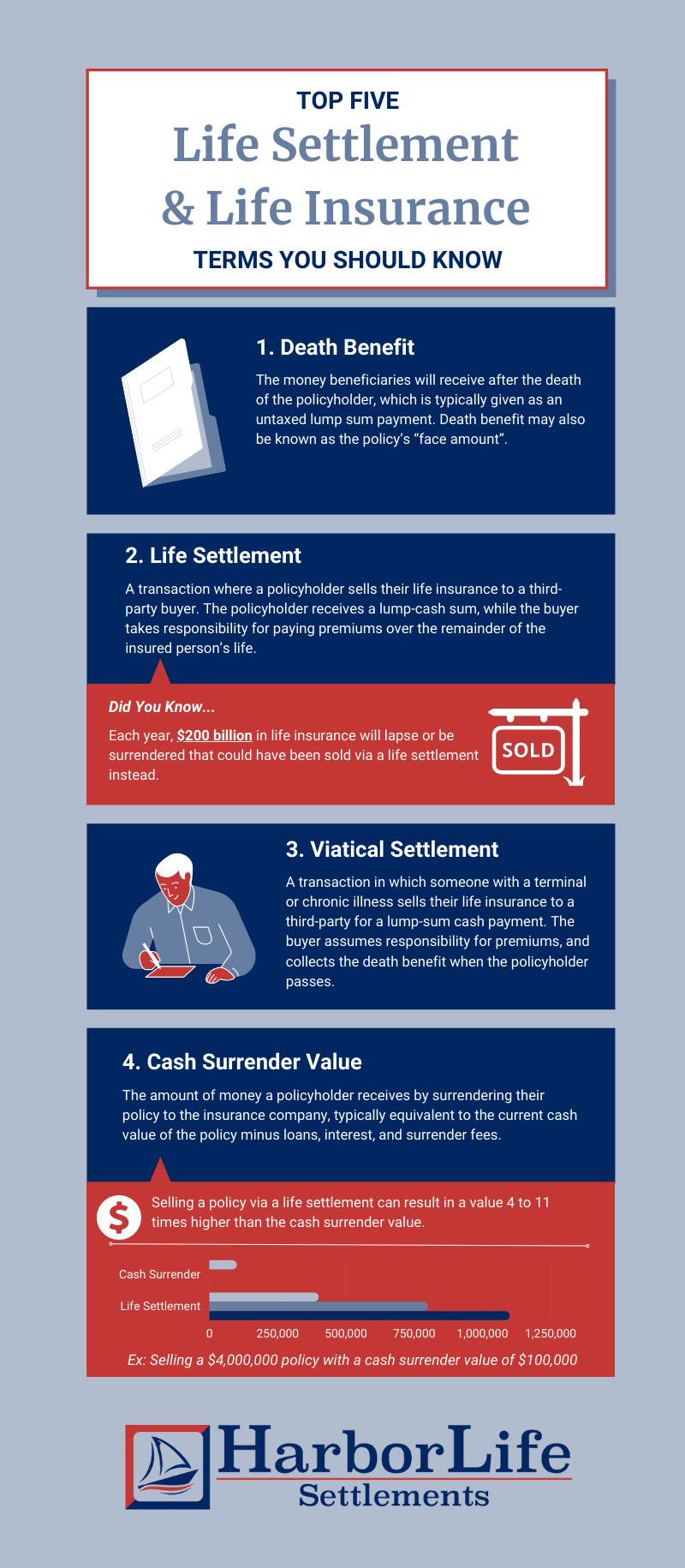

Cash Surrender Value: The amount of money a policyholder receives by surrendering their policy to the insurance company, typically equivalent to the current cash value of the policy minus loans, interest, and surrender fees.

Conversion Right: The right of eligible term life insurance policies to be converted into a form of permanent life insurance that accumulates cash value.

Coverage Period: The length of time a life insurance policy will provide coverage for the policyholder.

Death Benefit: The money beneficiaries will receive after the death of the policyholder, which is typically given as an untaxed lump sum payment. Death benefit may also be known as the policy’s “face amount”.

Direct Response: The direct sale of a life insurance policy by the insurer to an individual.

Disclosure Statement: A document that explains details of a life insurance policy to the individual it covers.

Dividend: A distribution of money to a policyholder that refunds a portion of premiums paid or rewards individuals based on the insurance company’s profits. Dividends may be available on whole life policies, though a return is not guaranteed.

Evidence of Insurability: Documentation that explains an individual’s physical health and financial details, which is used by an insurance company to determine if the individual is eligible for a life insurance policy. The information also helps insurers determine the level of risk for the individual, which affects the premiums that will be charged for coverage.

Face Amount: Face amount is another term for the death benefit, which is the amount of money the policyholder’s beneficiaries will receive after their death.

Final Expenses: A combination of expenses incurred at the time of someone’s death, typically including funeral costs and outstanding bills or debts. Policyholders may have the option to designate a portion of their life insurance death benefit to cover final expenses.

Fixed Amount Option: An option that allows death benefit proceeds from a life insurance policy to be paid through a series of fixed payments. The payments will continue in fixed increments until the base proceeds and earned interest run out.

Free Look Provision: A period of time (usually 10-30 days) that allows a newly insured individual to review their policy and return it to the insurer for a full refund if they are not satisfied.

Grace Period: A policy’s grace period is the length of time it will remain active after missing a payment, usually one month.

Guaranteed Universal Life Insurance: Guaranteed universal life insurance is a type of policy that offers fixed premiums that stay the same throughout the life of the policy.

InForce Illustration: An inforce illustration is an estimate of a life insurance policy’s cash value over time, based on current earnings and projected future costs.

Insurance Policy: A written contract between the policyholder and insurance carrier that indicates coverage details including who is included, the policy length, and terms of the death benefit.

Insured: The person is covered by the life insurance policy. The death benefit will be distributed to beneficiaries upon their passing.

Insurer: The company who issues the life insurance policy and pays the death benefit.

Lapse: A lapse occurs when the policyholder does not pay premiums to keep the policy in force. There is usually a 31-day grace period, but after that the policy will have to re-apply for coverage and may need to pay the unpaid premiums.

Life Expectancy: The projected lifespan of the policyholder based on medical records and comparisons to similar individuals.

Life Settlement: A transaction that involves a policyholder selling their life insurance policy to a third-party buyer. The policyholder receives a lump-cash sum, while the buyer takes responsibility for paying premiums over the remainder of the insured person’s life. After the insured dies, the buyer collects the death benefit.

Nonforfeiture Options: A life insurance policy provision that specifies how accumulated cash value can be used if the policyholder stops making payments. For example, cash value may be used to keep the policy intact after a missed payment.

Policy Loan: A loan from a life insurance company to a policyholder that uses the cash value as collateral.

Policy Owner: The party who owns the life insurance policy. This is not always the insured, as an insured individual can sell their policy to a third party through a life settlement which would make someone else the policy owner.

Premium: The cost of maintaining the life insurance policy throughout the insured individual’s life. Premiums are dependent on several factors including policy type, policyholder age, health status, and family history. They can be paid monthly, quarterly, semi-annually, or annually.

Provider: In a life settlement, a provider is a licensed third-party who is required to be part of the transaction by state regulators. They facilitate the transaction, and generally either resell the policy to an institutional investor or hold the policy to maturity.

Reinstatement: The option to re-activate a life insurance policy after it has lapsed due to a missed payment. Doing so may require the individual to start a new application for coverage, depending on the insurer and the length of the lapse.

Rider: An optional add-on to life insurance policies that offers extra benefits, usually for a higher premium than the base policy.

Surrender: The process of giving a life insurance policy back to the carrier, usually for a small return in the form of a lump-cash sum.

Term Life Insurance: An insurance policy that provides coverage for a specific period of time, typically between 1-30 years. At the end of the term, the policyholder can usually be renewed, but may cost more. Term policies do not accumulate cash value.

Underwriter: The individual who reviews a person applying for life insurance coverage, who decides whether the individual is insurable and at what rate they should be charged for coverage. An underwriter will also review individuals who are selling their policy to determine how much it is worth.

Underwriting: The process used to evaluate a person applying for insurance in order to determine the premiums for the individual. The process is also used for an individual selling a life insurance policy through a life or viatical settlement in order to determine how much the policy should be sold for.

Universal Life Insurance: A hybrid type of life insurance that combines the protection of term policies with the cash value elements of permanent insurance.

Variable Universal Life Insurance: A type of permanent insurance that features several sub-accounts with an investment component. The policyholder can select which accounts to put money into through their premium payments.

Viatical Settlement: A transaction in which someone with a terminal or chronic illness sells their life insurance to a third party for a lump-sum cash payment. The buyer assumes responsibility for premiums and collects the death benefit when the policyholder passes away.

Whole Life Insurance: A type of life insurance that covers someone through the remainder of their life. These policies also accumulate cash value, which can be used to help with retirement or leave behind a larger death benef